Latest News

November 1, 2017

By Jared Greene

Young, aggressive “FinTech” firms that are combining increasingly powerful computing resources with advanced algorithms to offer financial services are disrupting yesterday’s image of the buttoned-down, pinstripe-suited banker.

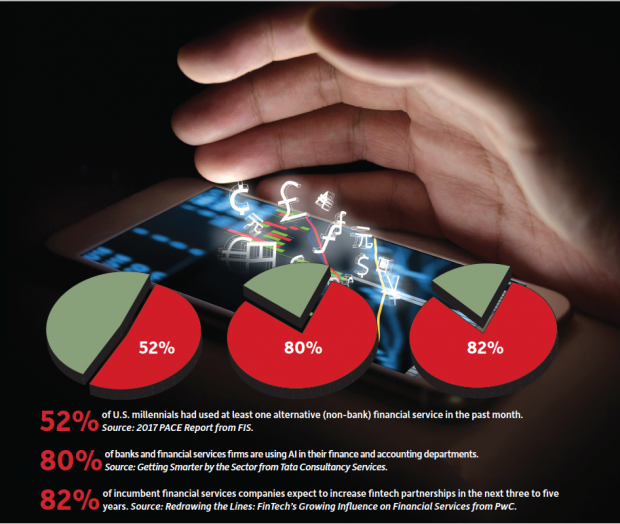

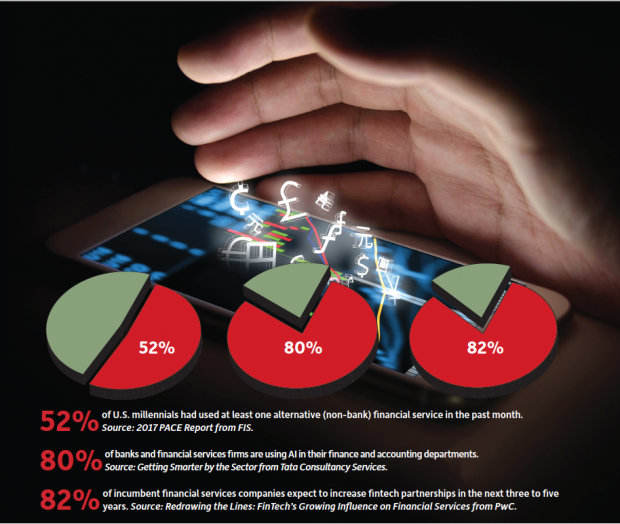

For example, according to the 2017 Performance Against Customer Expectations (PACE) Report from FIS, 52% of U.S. millennials had used at least one alternative (non-bank) financial service in the past month, and older millennials now earn more than baby boomers.

FIS is a financial services provider that was ranked first in the 2017 IDC FinTech Rankings, which categorizes and evaluates the top global providers of financial technology based on calendar-year revenues from financial institutions for hardware, software and or services.

Globally, the situation is much the same, according to the 2017 PACE Report. It shows that millennials and Gen Xers, especially, want a more advisory relationship with their banks, but less than a third have financial advisors.

“Banks must harness the new technologies across their global operations to increase efficiency, meet customer expectations and capture new opportunities,” notes The New Dynamics of Financial Globalization, a McKinsey Global Institute report. “Harnessing advanced analytics and machine learning algorithms to better understand risks in international markets could be a competitive edge.”

Large Banks Are Investing in AI

Although the 2017 PACE Report shows smaller banks are falling behind in digitalization efforts to meet demands of consumers and small- and medium-sized businesses, larger banks and financial services are leading the artificial intelligence (AI) charge. Last year, Tata Consultancy Services (TCS) surveyed 182 banks and financial services firms with average revenues of $26 billion. The IT services, consulting and business solutions organization found that 86% of banks and financial services are already using AI, and the remainder plan to use it by 2020.

“Four out of five banks and financial services firms are using AI in their finance and accounting departments,” states the report on TCS’ survey data titled, “Getting Smarter by the Sector: How 13 Global Industries use Artificial Intelligence.” Of the group using AI in finance and accounting, 72% of them are using AI in financial trading.

The report cites examples that include Goldman Sachs investing in analytics firm Kensho to use AI for analyzing unstructured data to spot trends, as well as Barclays PLC developing an AI system to let people talk to a device and get financial information. In addition to providing investment advice to clients, venture capital (VC) firms are investing in their own solutions to determine where to invest.

For example, CircleUp, a VC firm that focuses on consumer product-related companies, has an online platform called Classifier that “has evaluated more than 10,000 potential deals done by the firm’s analysts between 2011 and 2016,” according to the FIS report. “With Classifier, a team of less than 10 analysts can review 500 opportunities per month, versus the 500 evaluations per year done by the average private equity firm.” A book by three leaders of Cognizant’s Center for the Future of Work, What to Do When Machines Do Everything, cites Betterment, a company that uses AI to provide “personalized, curated wealth management services 24x7” as an example. According to the book, Betterment’s assets under management grew from $1.1 billion in 2015 to about $10 billion today by focusing on high earners who were not yet wealthy enough for traditional large banks to consider them as candidates for personal finance advisory services.

In September, Betterment accepted the support of two Wall Street stalwarts—Goldman Sachs and BlackRock—to offer new “smart-beta” portfolio options. The “smarts” in the option refer to algorithms that employ AI to look for factors that might improve stock performance.

The deal, which surprised the financial services industry, given Betterment’s anti-establishment outlook, may signal a trend. According to “Redrawing the Lines: FinTech’s Growing Influence on Financial Services,” a report from PwC, 82% of incumbent financial services companies expect to increase FinTech partnerships in the next three to five years. According to the PwC Global FinTech Survey 2017 survey, 45% of respondents are already partnering with FinTech companies, up from 32% last year.

As Betterment’s success shows, there is still plenty of room for AI expansion in the financial sector. For example, only 25% of TCS’ survey respondents use AI in a sales function, where it could help them decide who to extend loans to, or where to invest. The C-suite is also ripe for expansion, with just one in five banks using cognitive tools to assist with corporate level decision-making, according to the survey.

Regulatory Obstacles to Growth

However, government regulations are not keeping up with the advancements in financial technologies, leading to market uncertainties.

A November 2015 Silicon Valley Bank survey revealed FinTech company founders and investors expected regulatory issues to be the biggest impediment to their success in 2016. Nearly half of the survey respondents (43%) said regulatory issues were their biggest impediment, followed by reticence by corporations to adopt new technology (24%), changing consumer behavior (18%) and access to funding (15%).

The top regulatory barrier to innovation, according to 54% of PwC Global FinTech Survey 2017 respondents, revolved around data storage, privacy and protection. They identified digital identity authentication and AML/KYC (anti-money laundering/know your customer) compliance issues as the second and third most concerning barriers, at 50% and 48% respectively, according to the PwC report.

Here again, computing technology may come to the rescue with “RegTech” solutions that use Big Data analytics and AI to automate many regulatory compliance tasks (see page 24). Automating data collection, reconciliation, analysis, formatting and distribution tasks allows banks and financial services to meet strict compliance requirements and short deadlines. Some new RegTech solutions employ blockchain technology to speed the KYC onboarding process, for instance.

Investment banks traditionally maintain their own independent databases of transactions, customer information and other reference data. To complete transactions, banks need to reconcile and confirm their data with other parties. Blockchain technologies leverage advances in software, communications and encryption that will enable investment banks to move from maintaining a separate, fragmented database structure to a shared, distributed database that spans organizations. Blockchain technology supports a shared digital ledger of transactions recorded and verified across a network of participants. With the technology, transactions reside in a tamper-evident data structure that is said to provide the necessary levels of data security and access for each user.

A January 2017 report by Accenture and McLagan claims blockchain technology could reduce infrastructure costs for eight of the world’s 10 largest investment banks by an average of 30%, translating to $8 billion to $12 billion in annual cost savings for those banks.

The report, “Banking on Blockchain: A Value Analysis for Investment Banks,” finds that compliance costs could drop by 30% to 50% at the product level and on a centralized basis due to the improved transparency and auditability of transactions.

“Capital markets institutions have faced a perfect storm of regulatory-compliance costs and revenue pressures in recent years, prompting them to invest in emerging technologies as a lever to improve profitability,” said Richard Lumb, Accenture’s group chief executive, Financial Services.

More Info

Did You Know?

- Banking respondents to Tata Consultancy Services’ survey spent an average $77 million per company in 2015 on cognitive technologies. The median spend was $5 million. Seven of the 182 banks and financial services firms surveyed spent $500 million or more each on AI in 2015, with four of those spending at least $1 billion.

- Looking ahead to 2020, banks surveyed by Tata expect their investments in AI to increase to $99 million on average per company, a 29% increase over 2015.

- Both Gen Xers (age 37 to 51) and senior millennials (age 26 to 36) prefer digital banking, but do not yet have the mobile-first preferences of their younger counterparts, according to FSI’s 2017 PACE Report.

- Nearly two-thirds of senior millennials and half of Gen X have at least one major life event planned within the next two to three years, according to FSI’s 2017 PACE Report. Major life events include paying for tuition, starting a business, marriage, and buying or renovating a home. The financial services provider notes that banks can grow by reaching out to these customers via analysis of demographics, transactional and socioeconomic data within the banks’ systems.

- Widespread adoption and use of digital finance could increase the gross domestic products of all emerging economies by 6%, or a total of $3.7 trillion, by 2025, according to a McKinsey Global Institute (MGI) report: “Digital Finance for All: Powering Inclusive Growth in Emerging Economies.” “This is the equivalent of adding to the world an economy the size of Germany, or one that’s larger than all the economies of Africa,” states the research firm.

- “Behavioral analytics across compliance, fraud and cyberthreat detection/prevention will be in place in 15% of banks in 2017 to help avoid regulatory fines and sanctions,” according to IDC Financial Insights.

Jared Greene is a contributing editor of Digital Engineering.

Subscribe to our FREE magazine, FREE email newsletters or both!

Latest News